For years, the dominant model in the subscription economy centered around direct relationships between consumers and service providers. However, new data from Bango’s “Subscriptions Assemble” report, based on a survey of 5,000 U.S. subscribers, suggests that trend is changing.

For years, the dominant model in the subscription economy centered around direct relationships between consumers and service providers. However, new data from Bango’s “Subscriptions Assemble” report, based on a survey of 5,000 U.S. subscribers, suggests that trend is changing.

According to the study, 68% of U.S. subscribers now pay for at least one subscription through an indirect channel—such as a telco, retailer, or financial institution. Additionally, the average U.S. subscriber pays for 5.4 subscriptions, with two of those now bundled rather than purchased directly from a provider.

The findings indicate a growing preference for consolidation, cost savings, and convenience, with 62% of respondents stating they would rather have a bundle than manage multiple individual subscriptions.

- Younger consumers are leading this shift, with 41% of subscribers under 35 believing they get a worse deal when subscribing directly.

- Additionally, 44% of subscribers now get a subscription they previously paid for free through bundling, increasing to 55% among 18-24 year-olds.

This evolution is particularly evident in streaming, where services like Paramount+, Apple TV+, and Discovery+ are increasingly available through Amazon Prime Video or Verizon’s +play rather than through standalone subscriptions. The shift isn’t limited to entertainment—bundles now include financial, fitness, and AI services as well, with 9% of subscribers now paying for an AI subscription like ChatGPT.

‘Super Bundling’ and Subscription Fatigue

Despite this bundling boom, the report highlights subscription fatigue as a growing concern. While consumers want more subscriptions, they struggle with managing them across different platforms and providers.

- 63% of respondents want a single app to manage all of their subscriptions, a concept the report dubs “Super Bundling.”

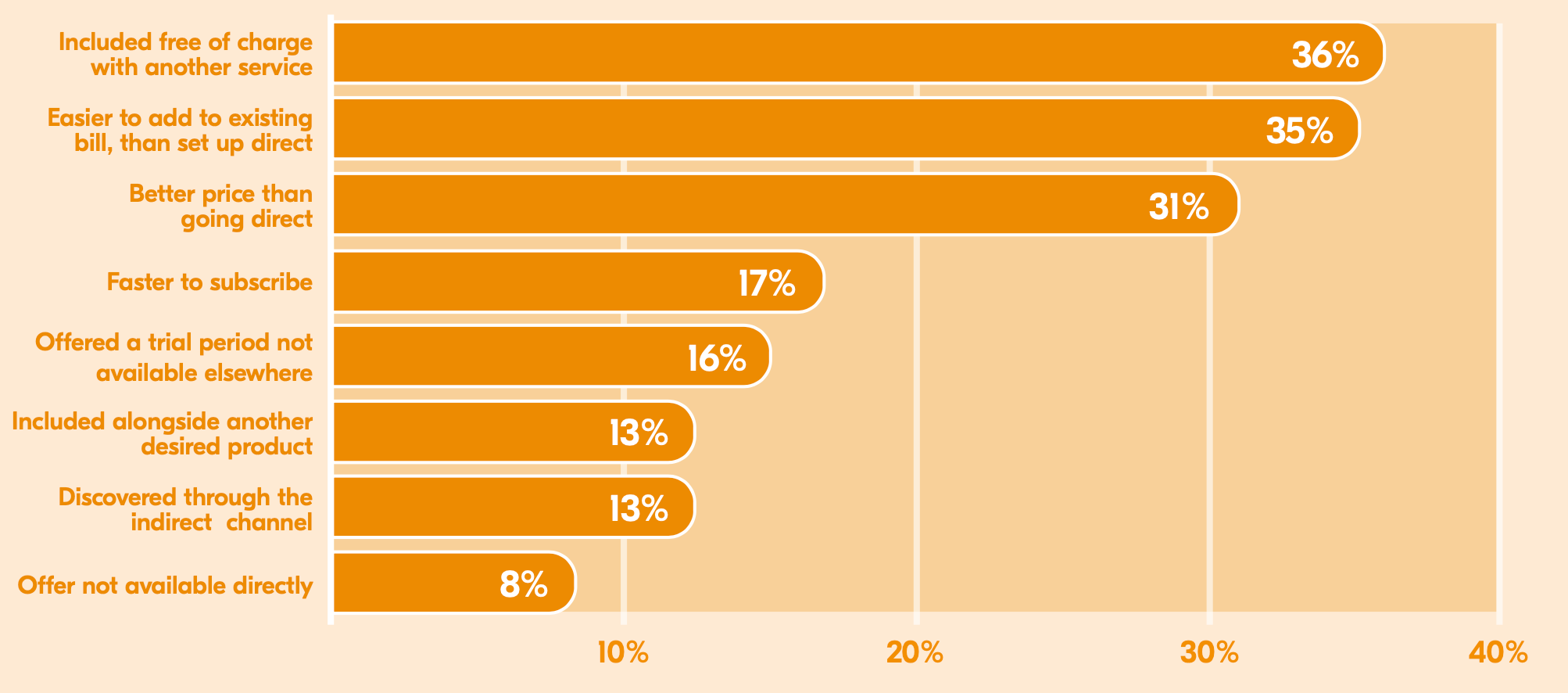

Telcos remain the dominant players in bundling, with 55% of respondents receiving at least one subscription through their mobile provider. However, other industries—particularly retailers (34%), payment platforms (23%), and even social media companies (19%)—are entering the subscription bundling space. The report suggests that platforms like Verizon +play are leading the charge toward centralizing subscriptions in one place.

INSIDER TAKE

The Business Implications of Subscription Bundling

The data confirms a growing shift toward indirect subscription models, but the key question for subscription businesses is whether bundling helps or hurts long-term revenue and retention.

Opportunities:

- Increased Reach: Bundling opens up access to new customers who might not have signed up directly.

- Stronger Retention: Consumers locked into a bundle may be less likely to churn individual services.

- Revenue Expansion: Partnerships with telcos, retailers, and financial institutions provide additional revenue streams beyond direct subscriptions.

Challenges:

- Loss of Direct Control: Subscription providers relying on third-party bundling lose direct relationships with subscribers, making it harder to influence retention and upselling.

- Pricing Pressure: With 28% of respondents believing direct subscriptions offer a worse deal, bundling could further erode standalone pricing power.

- Brand Dilution: If a service is bundled with several competitors, its differentiation in the marketplace could be diminished.

Bango CEO Paul Larbey positions the shift as moving beyond the “subscription economy” into the “bundle economy,” where platforms collaborate rather than compete. While this framing is beneficial to Bango’s business model, the sample size of 5,000 U.S. subscribers makes this a significant dataset worth paying attention to. Subscription businesses need to assess whether bundling aligns with their growth strategy and determine the right balance between direct and indirect customer acquisition.

The subscription economy is no longer just about acquiring and retaining subscribers—it’s about where and how consumers choose to subscribe. For many providers, bundling may be the key to staying relevant in an evolving market.